This article was originally published on September 6, 2023 on Forbes.com. Written by Peyton Carr.

As a startup founder, your journey to build a successful company not only benefits your customers but also holds the potential for significant personal wealth. However, with financial gains come tax implications that can impact your earnings. To maximize your wealth and protect your assets, it’s important to consider tax strategies and QSBS strategies for startup founders at different stages of your company’s life cycle. This article explores various tax optimization techniques tailored for startup founders, offering insights into reducing capital gains tax, minimizing state and federal tax, mitigating estate taxes, and safeguarding assets from creditors and legal disputes.

Tax optimization and advanced planning are multidimensional and continuous

Before delving into specific strategies, it’s crucial to grasp a fundamental understanding: Tax optimization and advanced planning are continuous processes, never a mere one-time project or strategy to get a tax break. At various times during your company’s life cycle, different opportunities will emerge, and post-exit, completely new opportunity sets present themselves. Tax laws and the federal tax code change, valuations fluctuate, and your own goals, net worth, family, and priorities shift over time. Thus, optimizing is an ongoing process that requires perpetual consideration.

Keep an eye on your equity value

Managing your equity ownership throughout the many stages of your company’s life cycle is a fundamental concept of tax optimization. By considering the value of your shares now and, more importantly, the timing and future expectations of the value of your shares, you can strategically plan for the different stages and tax and capital gains optimization opportunities that present themselves. Your personal circumstances and long-term goals can help guide your decisions in minimizing tax exposure and potentially saving millions.

Utilize qualified small business stock (QSBS)

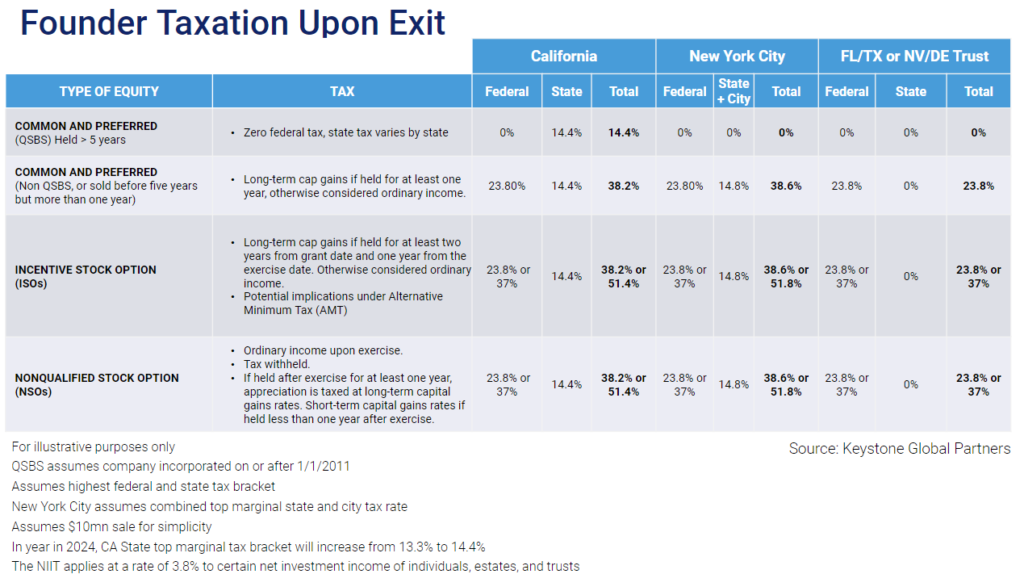

Qualified small business stock (QSBS) (read the QSBS rules), also referred to in the Internal Revenue Code Section 1202, offers a lucrative tax-saving opportunity for venture-backed domestic c corporation startup founders.

By excluding up to $10 million of the capital gain from tax upon an exit or sale, QSBS allows individuals who qualify, and some trusts, to reap substantial benefits. These tax benefits can create a tax savings of up to 23.8% for federal income tax purposes and, depending on the state, potentially additional state tax savings.

For a more detailed exploration of Qualified Small Business Stock (QSBS) and how it can potentially save you millions in tax, we recommend reading our in-depth QSBS Guide. This comprehensive guide will provide a deeper understanding of the QSBS rules, including the holding period, eligible shareholders, and the corporation’s assets and gross asset test. It is designed to help you to understand the tax opportunities that stockholders of qualified small businesses have.

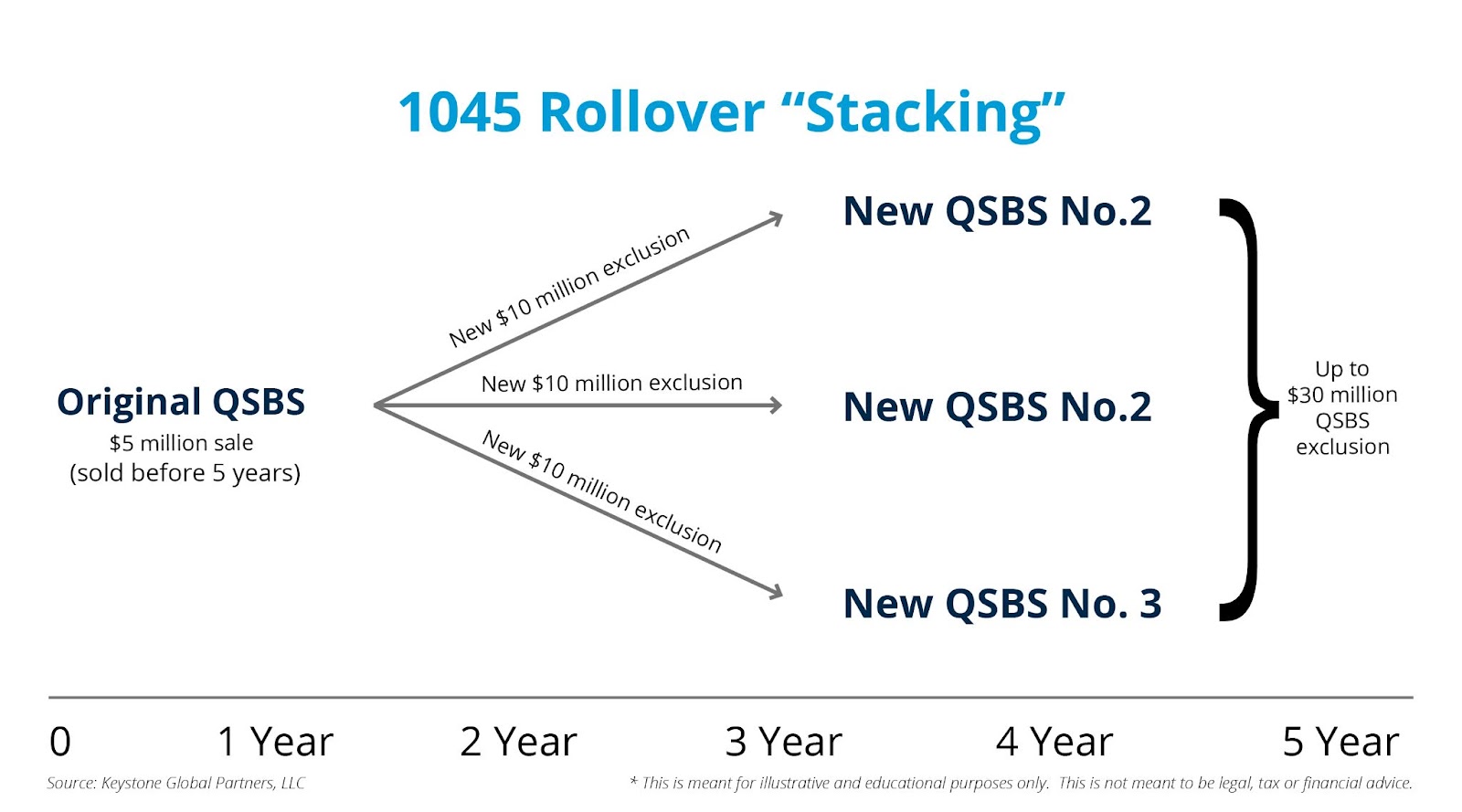

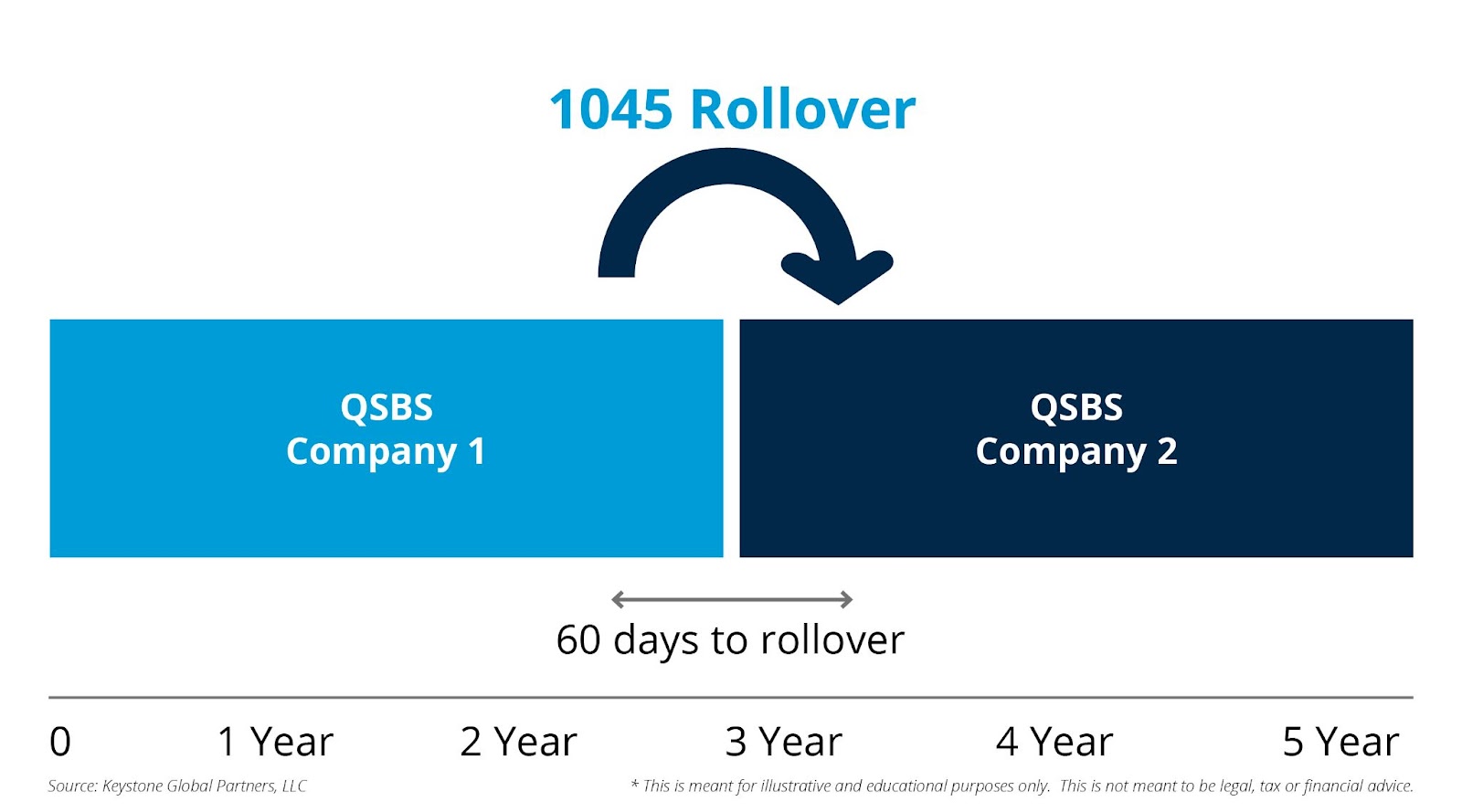

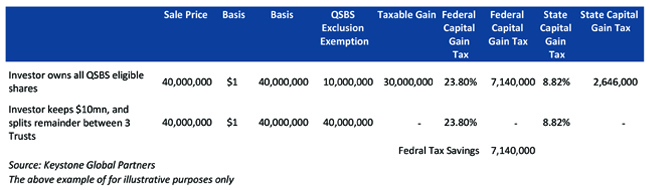

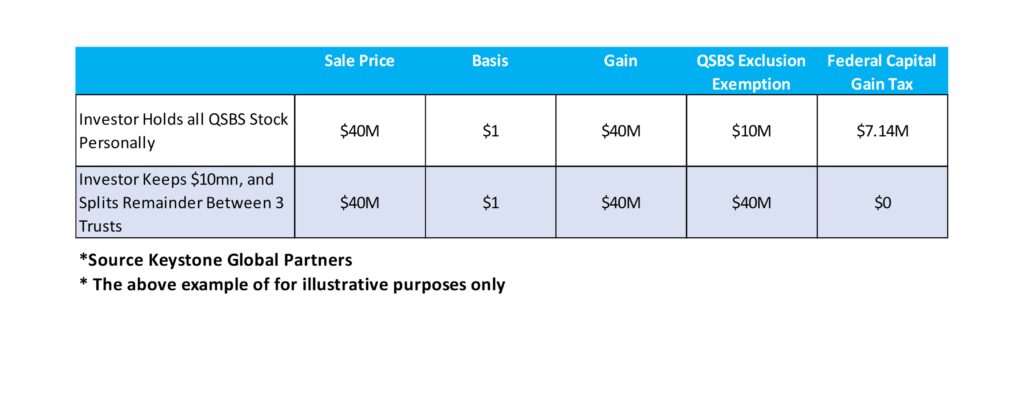

QSBS Stacking with a Non-Grantor Trust

To maximize or multiply the QSBS tax exclusion (QSBS Stacking), many founders consider gifting QSBS-eligible stock to irrevocable non-grantor trusts, qualifying the trusts for their own $10 million exclusions. An example of this would be a founder who sets up three trusts, one for each of their children as the trust beneficiaries and gifts $10 million of QSBS to each trust. There is now $40 million of QSBS gain exclusion. For example, properly structuring the trust in a tax-exempt state like Delaware, Nevada, or Texas can be an area of further tax optimization. The example below only takes federal tax into account.

Consider a parent-seeded trust for State Tax and Estate Tax Benefits

To plan for future generations and to minimize estate taxes and high state taxes, a parent-seeded trust can be an effective strategy. Created by the founder’s parents with the founder as the beneficiary, this trust allows the founder to sell shares to it, eliminating any gift tax but disqualifying the ability to claim QSBS. Distributions can be made to the founder at the trustee’s discretion, who is chosen by the founder. The advantage of this strategy lies in transferring all future asset appreciation out of both the founder’s and the parents’ estate, thereby safeguarding it from potential estate taxes in the future. The trust’s location in a tax-exempt state reduces state-level taxes, resulting in substantial tax savings.

Transfer the upside and reduce future estate taxes with a GRAT

For founders with significant “unicorn” positions and limited lifetime gift tax exemption, a grantor retained annuity trust (GRAT), or a few of them, can be a powerful strategy by transferring assets outside of their estate without using up their gift tax exemption or being subject to gift tax. Founders can minimize their future gift and estate tax exposure by transferring their equity’s upside into a trust for their beneficiaries. To execute, the founder (referred to as the grantor) initiates the process by transferring assets into the GRAT, thereby receiving a series of annuity payments in return. Calculating these annuity payments takes into account the tax code IRS 7520 rate. If the equity goes up in value during the GRAT term, this equity upside stays with the trust, gift tax- and estate tax-free.

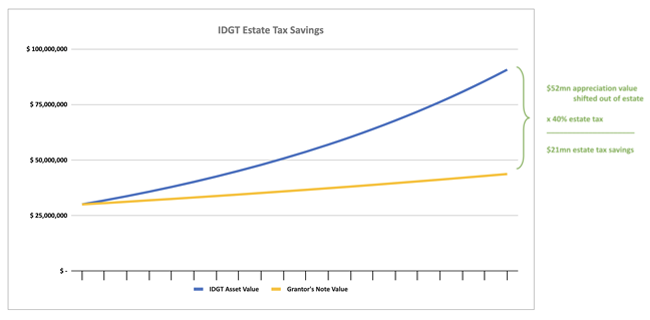

Get greater flexibility in wealth transfer with IDGT

The intentionally defective grantor trust (IDGT) offers similar benefits to the GRAT in minimizing estate tax exposure. However, it requires the grantor to seed the trust with 10% of the asset value, utilizing some lifetime gift exemption. The remaining 90% is sold to the trust in exchange for an interest-only note. Since it is interest only, the payments are much lower than the above GRAT strategy annuity payments. The IDGT also provides more flexibility and the option for generation-skipping transfers, making it a superior choice for those aiming to avoid generation-skipping transfer tax (GSTT).

Conclusion

Tax optimization can play a significant role in steering your personal wealth journey as a founder. As you explore the various tax savings strategies such as QSBS, GRAT, Parent Seeded Trust, or IDGT outlined above, remember that many can be combined or implemented at different junctures within your company’s life cycle. What I’ve covered here merely scratches the surface of the tax benefit achieved, and many other exit planning strategies exist that are not mentioned. In the end, this is all highly customized based on your own opportunity set, and there is no one-size-fits-all strategy.

I recommend you devote thoughtful consideration to your equity ownership and its fair market value, the evolving stages of your company, and your own unique goals. Given the intricacies involved, these strategies require professional counsel (attorneys, tax advisors) and careful planning.

Disclaimer

The information and opinions provided in this material are for general informational purposes only and should not be considered as tax, financial, investment or legal advice. The information is not intended to replace professional advice from qualified professionals in your jurisdiction.

Tax laws and regulations are complex and subject to change, and their application can vary widely based on the specific facts and circumstances involved. You can reference the Internal Revenue Services website here to learn more about federal tax. Any tax information or advice in this article is not intended to be, and should not be, used as a substitute for specific tax advice from a qualified tax professional. You should consult with a licensed professional for advice concerning your specific situation.