Imagine maximizing your profits from your startup’s exit through a few strategic tax break strategies and the Qualified Small Business (QSBS) rules. For founders holding substantial positions of QSBS, this dream could become a tangible reality. By harnessing the often overlooked but powerful tax benefits of QSBS and QSBS Stacking, you may be able to enhance your post-exit take-home.

Quick recap: Qualified Small Business Stock refers to a tax provision under Internal Revenue Code Section 1202, which offers entrepreneurs significant tax benefits, potentially allowing for the exclusion of up to $15 million ($10 million for shares issued before July 4, 2025) or 10 times the basis, whichever is greater, from taxes. Wondering if you qualify? You can read our article on whether you’re eligible for Qualified Small Business Stock (QSBS), covering founder stock, the Section 1202 Exclusion, and how to qualify.

In this guide, we will discuss the tax benefits of QSBS stacking, an advanced strategy for multiplying the QSBS exemption, and we’ll examine a variety of strategies specifically designed for QSBS stacking. We will interchangeably use the terms QSBS exclusion and QSBS exemption. Many refer to the QSBS exclusion as the QSBS exemption, even though QSBS exclusion is the accurate term.

Important Context, Key Law Changes & QSBS Rules under OBBBA

While Qualified Small Business Stock (QSBS) planning and “stacking” strategies can be powerful when executed correctly, they are also highly technical. Each strategy’s outcome depends on the specific facts, timing, trust structure, and evolving IRS and legislative guidance. The concepts outlined here are intended for educational purposes and should be evaluated with tax and legal advisors familiar with §1202 and related trust-planning provisions.

This article was revised on October 14th, 2025. The update incorporates the latest post-OBBBA Qualified Small Business Stock (QSBS) rules. These new rules enhance QSBS eligibility by expanding the gross asset test eligibility ceiling from $50 million to $75 million and increasing the individual benefit limit from $10 million to $15 million. Additionally, the QSBS exclusion holding period will now be introduced in stages: a 50% exclusion for a three-year holding period, 75% for four years, and a full 100% after five years. It is crucial to note that these specific adjustments apply exclusively to shares issued after July 4, 2025.

Coordinating Old and New QSBS

If you hold both pre-OBBBA QSBS (acquired on or before July 4, 2025) and post-OBBBA QSBS (acquired after that date) in the same company, the law requires a single aggregated exclusion limit per issuer. In other words, you cannot claim both the $10 million and $15 million limits separately for the same company. However, separate limits still apply to different issuers and to different taxpayers (for example, family members or non-grantor trusts created through stacking, which we’ll cover below). Founders should carefully track issuance dates and collaborate with tax counsel to model which shares qualify under each regime when planning a sale.

When to Implement QSBS Stacking (Timing Strategy)

Understanding timing in the context of when to engage in this type of exit planning is crucial for any startup founder with an exit on the horizon. Ideally, the optimal window is when an exit seems not only possible but probable, and certainly well in advance of when a formal offer has been accepted.

Delaying your planning until you have a deal could lead to an unintended, hefty tax liability through the IRS assignment of income doctrine. The Internal Revenue Code states that if all contingencies have been addressed and cleared before the closing date, the transaction’s effective date is usually the signing date, not the closing date. Therefore, being proactive and not waiting until the last minute is crucial.

Top QSBS Stacking Strategies for Founders

1. Outright Gifting of QSBS

Founders looking to maximize their QSBS exemption might consider gifting their Qualified Small Business Stock (QSBS) outright to non-spousal family members, such as children, parents, or other qualifying individuals as one QSBS stacking approach. This method of donative transfer enables the recipient to maintain the original QSBS holding period of the founder while securing their own $10 million (or $15 million if the shares were acquired after July 4, 2025) exclusion. For example, if you have $20 million of QSBS acquired before July 4, 2025, and you gift $10 million to your brother, you have created an additional $10 million of exclusion, resulting in a total of $20 million exempt from federal taxation.

However, what outright gifts gain in simplicity, they lack in other important areas, such as control, protection against creditors, and efficient utilization of your lifetime gift & estate tax exemption. These items are why we typically do not recommend this QSBS stacking approach.

Valuation Risk and Gift Undervaluation

When gifting QSBS shares, especially close to a financing round or liquidity event, the IRS expects a defensible fair-market-value appraisal. If the company’s value rises sharply or an acquisition is announced soon after a gift, the IRS may argue that the shares were undervalued, potentially using up more of your lifetime gift and estate-tax exemption or creating an unexpected gift-tax liability. To mitigate this, founders should obtain a qualified appraisal from a valuation professional and file a Form 709 gift-tax return with adequate disclosure. Doing so starts the statute of limitations on valuation challenges and provides a documented basis for the transfer.

Key Considerations When Gifting or Using Trusts

While gifting QSBS to family members or irrevocable non-grantor trusts can, in theory, allow multiple taxpayers to each claim their own QSBS exclusions, this strategy must be executed with precision. Each trust must qualify as an independent taxpayer, maintain distinct beneficiaries and governance, and avoid being treated as a “grantor” or “collapsible” trust under IRS aggregation doctrines.

Overly similar or “cloned” trusts have been challenged by the IRS under substance-over-form principles. Therefore, these structures require thoughtful drafting, independent trustees, and strong documentation of purpose beyond tax benefits.

2. Irrevocable Non-Grantor Trust(s)

Company founders may explore a more advanced QSBS stacking approach: gifting QSBS to irrevocable non-grantor trust(s). This allows the trust(s) to qualify for its own $10 million or $15 million QSBS tax exemption. As the trust grantor, the founder chooses beneficiaries, such as children or future children, for example. When implementing this strategy, it’s crucial to note that if multiple trusts appear too alike, they might be viewed as a single entity for tax purposes. Under Treas. Reg. §1.643(f) (final rules effective 2023), the IRS can aggregate multiple trusts with the same grantor or beneficiaries if they are substantially alike and a principal purpose is tax avoidance. To reduce risk, trusts should differ in structure, trustee, timing, or beneficiaries. Simply put, if you intend to create several trusts, they should not be carbon copies of one another. Also, It is crucial for these trusts to be classified as non-grantor trusts rather than grantor trusts. If the founder retains specific powers or is considered the owner for income tax purposes, the Qualified Small Business Stock (QSBS) exclusion will be attributed to the founder rather than to the trust.

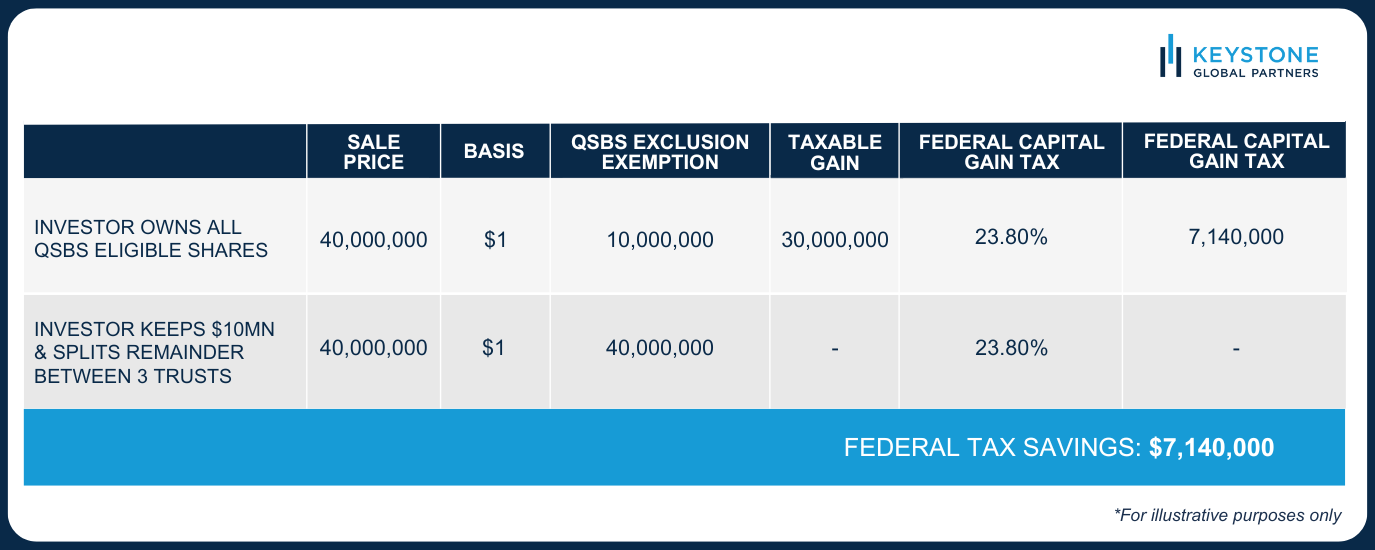

Consider a scenario where a founder has three children and owns qualified small business stock (QSBS) acquired before July 4, 2025. The founder sets up a QSBS non-grantor trust for each child and transfers $10 million of QSBS to each trust. By doing so, the founder effectively utilizes QSBS to exempt a total of $40 million from federal tax: $10 million for themselves through their personal exclusion and $30 million for the trusts. Refer to the example provided below.

The trust planning for founders example below assumes ideal conditions and simplified facts. In practice, valuation, timing of gifts, and the number and independence of trusts all affect whether each exclusion will be respected. Aggressive gifting or transfers made near a pending sale can be re-characterized as assignment of income or step transactions by the IRS.

Along with the federal tax benefits, it is essential to consider the potential advantages provided by state taxes. By establishing the trust in a tax-friendly state like Nevada, for example, there is a possibility of minimizing state taxes post-exit. It is also worth noting that while some jurisdictions, such as New York, conform to the federal tax treatment of QSBS, while other states like California do not.

When gifting QSBS shares to a trust, it is important to consider that this transaction will use a portion of your lifetime gift tax exemption, which is currently $13.99 million (or $27.98 million for married couples). This exemption is set to increase to $30 million, or $15 million per person, in 2026. Strategically, it’s advisable to make this move well in advance of an exit when asset valuations tend to be lower instead of waiting until the exit is imminent. By taking this approach, you can maximize the efficiency and utilization of your lifetime gift tax exemption.

3. GRAT Structure: Gift of the Remainder Interest

A Grantor Retained Annuity Trust (GRAT) provides founders with a tax-efficient approach to transfer assets to beneficiaries, effectively reducing gift and estate tax obligations. By placing assets into a GRAT, the founder is entitled to a series of annuity payouts determined by the IRS Section 7520 interest rate. If the assets grow at a faster rate than the interest rate, any excess amount will be retained in the trust. After the trust’s term expires, this excess can be transferred to the beneficiaries tax-free. This excess, referred to as the remainder interest, could qualify for Qualified Small Business Stock (QSBS) status if transferred to another person (excluding the grantor) or to a non-grantor trust.

This method of QSBS stacking is particularly attractive for founders who have maxed out their lifetime gift tax exemptions. However, the founder must outlive the trust’s term. Otherwise, the benefits are lost, and the assets return to the founder’s estate. If you’re considering this approach, it’s important to weigh the benefits with the limitations. Also, because GRATs are typically grantor trusts during the term, any sale inside the GRAT is taxed to the grantor. Only after the term, when the remainder passes to non-grantor status, can those shares be eligible for a new QSBS exclusion.

4. Using a CRUT (Charitable Remainder Unitrust)

Another strategy for leveraging the QSBS exemption and QSBS stacking involves a Charitable Remainder Unitrust. By transferring shares into a Charitable Remainder Unitrust, also known as a CRUT, the CRUT can potentially secure its own ten or fifteen-million-dollar QSBS exemption. This also provides the founder with a small deduction for their charitable contribution.

The founder then receives annual “unitrust” distributions from the CRUT, calculated by applying a fixed percentage to the value of the CRUT’s assets. Specific guidelines and the trust’s timeline determine this percentage, which typically ranges from 5% to 50%. The shorter the term, the greater the annual distributions to the non-charitable beneficiary; at the end of the term, the remaining assets pass to the charitable remainder beneficiary.

The tax-exempt status associated with a CRUT allows a founder to avoid immediate taxation when their shares are sold during an exit. While the founder will eventually face taxes on disbursements from the CRUT (assuming they are the CRUT beneficiary), these payments are typically subject to a tiered tax structure that prioritizes the distribution of the most heavily taxed segments first. However, if the CRUT meets the criteria for the Qualified Small Business Stock (QSBS) exclusion, a staggering $10 million or $15 million in gains from the exit could potentially be excluded from taxation when distributed back to the founder or CRUT beneficiary.

It remains unsettled whether a CRUT distribution of an excluded QSBS gain is taxed or remains tax-free. Although many tax advisors believe the gain retains its exclusion status, the IRS has not ruled on this. Proceed with caution and confirm with tax counsel.

Caution: Using GRATs, CRUTs, and Other Advanced Vehicles

Although techniques such as Grantor Retained Annuity Trusts (GRATs) and Charitable Remainder Trusts (CRUTs) can sometimes be integrated into QSBS planning, they introduce additional complexity. Qualification for the QSBS exclusion depends on nuanced factors such as the trust’s tax status, timing of transfers, and the ordering of distributions under the trust’s governing instrument.

For example, while a CRUT may hold QSBS, the tax benefits ultimately depend on the character of the income distributed to beneficiaries, which may differ from the underlying gain recognition at the trust level. Founders should evaluate these strategies with both estate and charitable planning counsel.

State Tax and Practical Considerations

While QSBS exclusions apply at the federal level, state income-tax treatment varies widely. Several states, such as California, Pennsylvania, Mississippi, and New Jersey (historically until 2026), do not conform to Section 1202 and will still tax QSBS gains. Others, like Hawaii and Massachusetts, only partially conform. Even in QSBS state tax conformity states, such as New York, trust residency and beneficiary location can affect how gains are taxed. For example, a non-grantor trust property formed in Delaware or Nevada may avoid state income tax. However, if its beneficiaries live in California, the California Franchise Tax Board may still tax the distributed income. Founders should coordinate with tax counsel to evaluate state-of-residency rules, trust situs, and post-exit relocation timing before executing stacking or trust strategies.

Conclusion

Founders with Qualified Small Business Stock (QSBS) have a variety of strategic choices to consider. By exploring strategies such as QSBS stacking, the tax code, and adhering to the QSBS rules, founders can optimize their after-tax results. QSBS stacking is just one of multiple sophisticated planning strategies to help reduce capital gains tax, lower future estate tax, and enhance asset protection. Implementing strategic QSBS solutions can further refine these approaches, maximizing benefits and aligning them with personal financial goals. Explore our guide for more insights on advanced tax-saving strategies tailored for company founders.

Approaching tax strategies requires careful financial planning and collaboration with tax advisors, legal experts, and wealth management professionals to ensure alignment with your individual circumstances and goals. These strategies are complex and depend heavily on specific facts. The IRS provides limited guidance on trust stacking, and aggressive structures may attract scrutiny. It is crucial to consult with tax, legal, and valuation experts before executing any strategy.

Read more about this subject in our published article written by our cofounder, Peyton Carr, on Forbes.com.

FAQs

How does QSBS stacking work?

QSBS stacking is a strategy that leverages the Qualified Small Business Exemption under Section 1202 of the Internal Revenue Code. This exemption allows a shareholder to exclude capital gains of up to $10 million (or $15 million if the stock is acquired after July 4, 2025) or ten times the stock’s basis, whichever is greater.

The objective of the stacking strategy is to increase the total cumulative limit of $10 million or $15 million by creating additional QSBS exclusions. This is done by transferring QSBS-eligible shares to different taxpayers or qualifying trusts (such as non-grantor trusts). Each recipient or trust then may qualify (if structured properly) for a new and separate exclusion.

What disqualifies QSBS?

Several factors can disqualify QSBS, or a stock from being considered Qualified Small Business Stock (QSBS) under Section 1202 of the Internal Revenue Code. Firstly, the stock must be issued by a domestic C corporation. Also, at the time of issuance, the company’s gross assets must not exceed $50 million. The company must use at least 80% of its assets in active qualified trade or businesses in specific sectors. The taxpayer that owns the QSBS must hold it for at least five years and have acquired it directly from the company. Lastly, certain types of redemptions where the company buys back shares from a shareholder or related person can disqualify QSBS. Learn more about QSBS eligibility here.

Are QSBS Stacking and Packing the same?

No, QSBS stacking is designed to increase and multiply the $10 million or 15 million QSBS exemption by generating additional taxpayers. QSBS Packing, on the other hand, is a tax strategy aimed at boosting your QSBS exemption above $10 million or $15 million by increasing the basis of your QSBS stock.

How many trusts can I use for QSBS Stacking?

There’s no specific limit in the tax code on how many trusts can be used for QSBS stacking, but each trust must be a truly separate taxpayer with distinct beneficiaries, grantors, and purposes. In practice, founders often create several non-grantor trusts (commonly 2–5) for family members or other beneficiaries, so that each can claim up to its own $10 million (or $15 million for shares acquired after July 4, 2025) QSBS §1202 exclusion.

The IRS has approved multiple-trust structures in private letter rulings when they were formed correctly and not created solely to avoid taxes. However, if trusts are too similar or established too close to a liquidity event, the IRS may apply the step-transaction or substance-over-form doctrines to collapse them into one taxpayer.

In short, there’s no hard cap, but quality and independence of structure matter far more than quantity. Each trust must have legitimate estate-planning or gifting intent, not just tax avoidance, to withstand IRS scrutiny.

When should founders consider QSBS stacking?

Founders should start planning early to optimize their use of the lifetime gift and estate tax exemption and reduce the risk of IRS step-transaction scrutiny. In most cases, this planning should begin 12–24 months before a potential exit. If a liquidity event moves faster than expected, it’s crucial to act before signing a Letter of Intent (LOI) and certainly before finalizing a sale.

Establishing non-grantor trusts well in advance can help minimize gift-tax exposure and preserve multiple §1202 QSBS exclusions across family members or beneficiaries. The bottom line: the earlier the planning begins, the greater the potential tax benefits and protections.