This article was originally published on November 8, 2021 on TechCrunch.com. Written by Peyton Carr.

The tax code includes provisions designed to encourage innovation and entrepreneurial risk-taking, particularly in the technology startup space. One such provision is the Qualified Small Business Stock (QSBS) under Section 1202. This enables founders, investors, and venture capitalists to avoid capital gains tax entirely if specific criteria are met.

However, many founders and investors face challenges when timing the sale of their businesses, often falling short of the five-year ownership requirement for QSBS tax savings. Fortunately, a 1045 rollover provides an opportunity to defer gains under certain conditions and allows individuals to salvage potential tax benefits.

What is a Section 1045 Rollover?

A 1045 rollover, also referred to as a QSBS rollover or 1045 exchange, allows founders or stockholders to defer capital gains taxes from the sale of QSBS. This is possible as long as those proceeds are reinvested into a new qualified QSBS within a specific timeframe.

Key Opportunities with a Section 1045 Rollover

Tax Deferral Flexibility

A 1045 exchange/1045 rollover allows you to defer taxes by reinvesting sale proceeds into replacement QSBS. If the combined holding period (original + replacement QSBS) meets the five-year mark and other rules are adhered to, you can avoid capital gains taxes on up to $10-million per taxpayer or 10x your tax basis, whichever is greater. Otherwise, taxes come due when the replacement QSBS is sold.

No Loss of Holding Period

One of the most significant benefits of a 1045 rollover is that it preserves the original QSBS holding period. This allows you to count it toward the required five-year period for tax exclusion. You’ll avoid starting the clock over when reinvesting in a QSBS-eligible company.

Multiplying Benefits

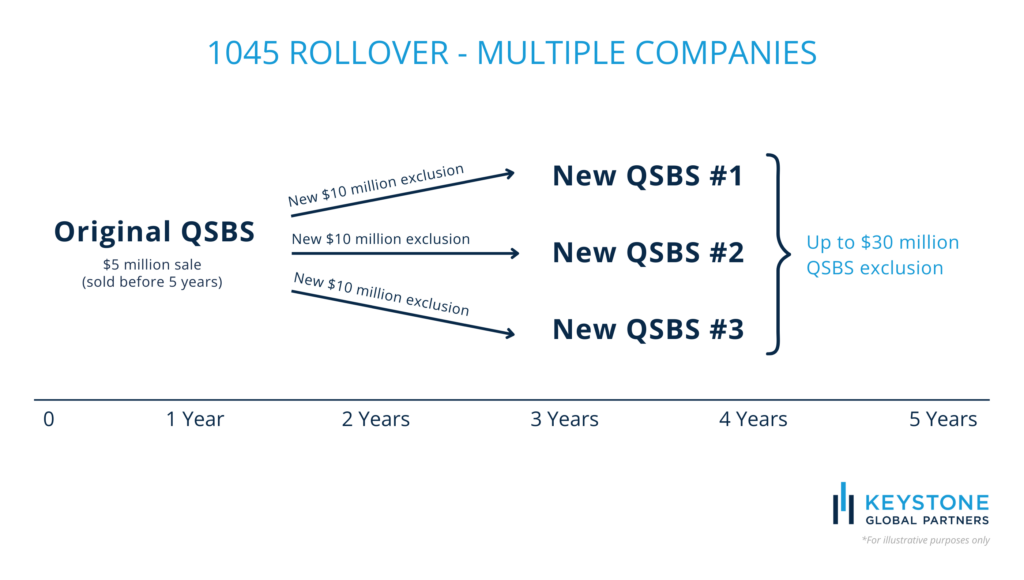

A 1045 rollover/1045 exchange enables investors to maximize the $10 million QSBS tax exclusion across multiple companies. By reinvesting proceeds into several new QSBS-qualified investments, investors can significantly enhance their tax benefits.

Investors are allowed up to $10 million or 10x their basis per taxpayer, per company. This offers a significant opportunity to maximize the total exemption amount and shorten the five-year holding period for the new investment.

Qualifications for a Section 1045 Rollover

To qualify for a Section 1045 Rollover, you must meet specific requirements:

- Initial QSBS Ownership: The original QSBS must qualify under Section 1202 and have been held for more than six months before the sale.

- Replacement QSBS: The replacement stock must meet QSBS qualifications both when purchased and during its holding period.

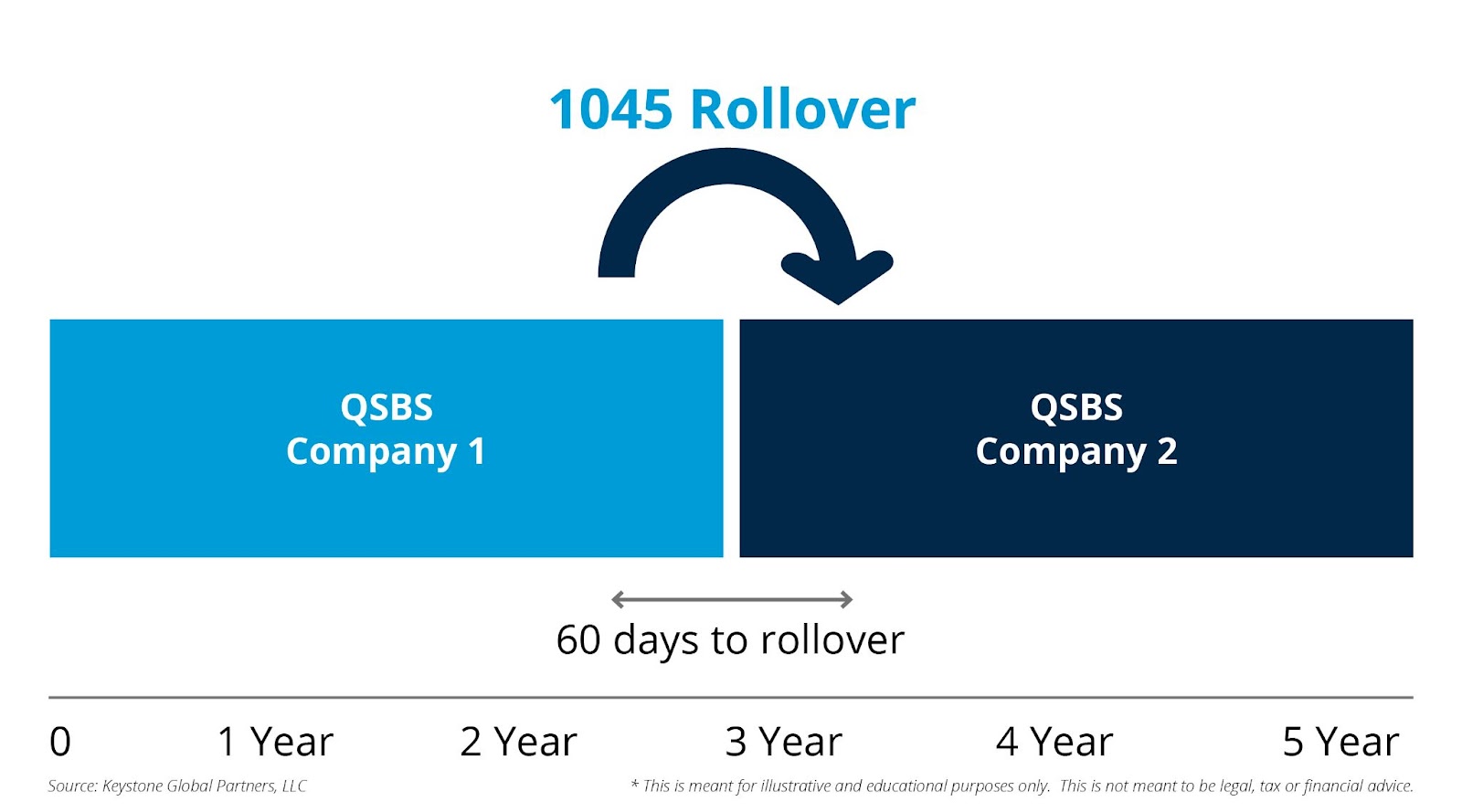

- 60-Day Rollover Period: Sale proceeds must be reinvested in replacement QSBS within 60 days of the original sale.

- Pro-Rata Rule: To defer 100% of the gain, you must reinvest 100% of the sale proceeds. Partial reinvestment only defers a proportional amount of the gain.

- Intent: Merely “parking” funds in a new corporation without genuine business activities is unlikely to withstand IRS scrutiny.

Strategies for Founders Using a 1045 Rollover

Reinvest in Other Startups

Founders leveraging a 1045 rollover can roll their sale proceeds into new QSBS-eligible startups. For instance, a founder who exits their company for $5 million can reinvest into three startups to potentially secure up to $30 million of QSBS exclusions. However, it’s important to ensure these new investments align with your goals rather than chasing tax benefits.

Acquire QSBS Companies

You could set up a new C-corp and use your 1045 rollover to move your sales proceeds into the newly established C while searching for QSBS companies to acquire. This method creates added flexibility if the acquisition timeline takes longer than 60 days.

Remember that for QSBS to apply, the holding period of the actively engaged new company must be at least 80% of the total holding time period. This also includes the search time frame for a new business.

Start a New Venture

For founders eager to launch a new business, forming a C-corp for their next venture allows them the advantage of a 1045 rollover. You can choose to move proceeds, defer taxes, and tack on the holding period from the original QSBS to the new QSBS.

This approach can offer some additional optionality. If the business fails, you can wind down the company and potentially exclude the capital gain from the original QSBS on any returned funds. This depends on the combined holding period, which consists of the new and initial holding periods and must exceed five years in total.

Timeline Considerations for Section 1045 Rollover

A Section 1045 rollover election is tied to the tax return for the year the original stock is sold. Timely action is crucial:

- 60-Day Rule: Reinvestment into new QSBS must happen within 60 days of selling the original QSBS.

- Holding Periods: The original QSBS must have been owned for at least six months, and the replacement QSBS must be held for six months or more to qualify for the deferral on the original sale.

- Reporting: The 1045 rollover election is made on the tax return for the year the original QSBS is sold, not when the rollover occurs if it happens in a future year.

Final Thoughts on a 1045 Rollover

The intent behind section 1045 and QSBS is to reward innovation, job creation, and entrepreneurship. For founders and investors, these provisions encourage reinvestment in the startup ecosystem while providing tax savings. That said, the 1045 rollover strategies outlined above require careful planning and collaboration with legal and tax professionals to ensure compliance.

If you’re thinking about utilizing a section 1045 rollover, be sure to consult with your advisors to ensure it aligns with your broader financial objectives. By exploring these sophisticated strategies, you can potentially maximize tax benefits while continuing to pursue your goals.