Navigating the tax landscape for startup founders and investors is complex. However, the Section 1202 gain exclusion provides a significant benefit: excluding gains from the sale of Qualified Small Business Stock (QSBS).

The 1202 exclusion can be transformative with proper planning. To effectively leverage this benefit, it is essential to understand the mechanics and strategies for maximizing the Section 1202 gain exclusion.

This article outlines many methods we use with our founder clients. You’ll learn how we maximize the Section 1202 gain exclusion for those with exits exceeding $10 million per taxpayer.

Understanding the Section 1202 gain exclusion cap

The Section 1202 gain exclusion permits taxpayers to exclude gains from selling Qualified Small Business Stock (QSBS), provided they meet specific eligibility criteria. The 1202 exclusion is subject to two main caps:

- The $10 Million Cap: This cap limits the Section 1202 gain exclusion to $10 million per taxpayer, per issuer, minus any previous exclusions for the same issuer.

- The 10X Basis Cap: Alternatively, the Section 1202 exclusion can be up to 10 times the taxpayer’s tax basis in the QSBS sold during the year.

Key aspects of the cap on the Section 1202 gain exclusion

Each taxpayer receives a separate exclusion cap for each issuing corporation. If you hold Qualified Small Business Stock (QSBS) in three companies, you qualify for a Section 1202 gain exclusion of $10 million or ten times your tax basis from each company. The total potential 1202 exclusion amounts to $30 million for this example.

Meanwhile, married couples are generally treated as a single taxpayer in regards to the Section 1202 gain exclusion cap. However, some argue that each spouse should be entitled their own separate exclusions.

Taxpayers with basis in their QSBS may benefit from the 10X basis cap. In contrast, founders and early employees who typically have low basis stock, use the $10 million cap. It is important to choose the greater value between $10 million or 10 times the basis.

Strategies for maximizing the Section 1202 gain exclusion: Stacking, packing, and tacking

Given the potential for substantial tax savings, smart founders often seek to maximize their available Section 1202 gain exclusions. Here are some of the more common approaches we implement with our founder clients.

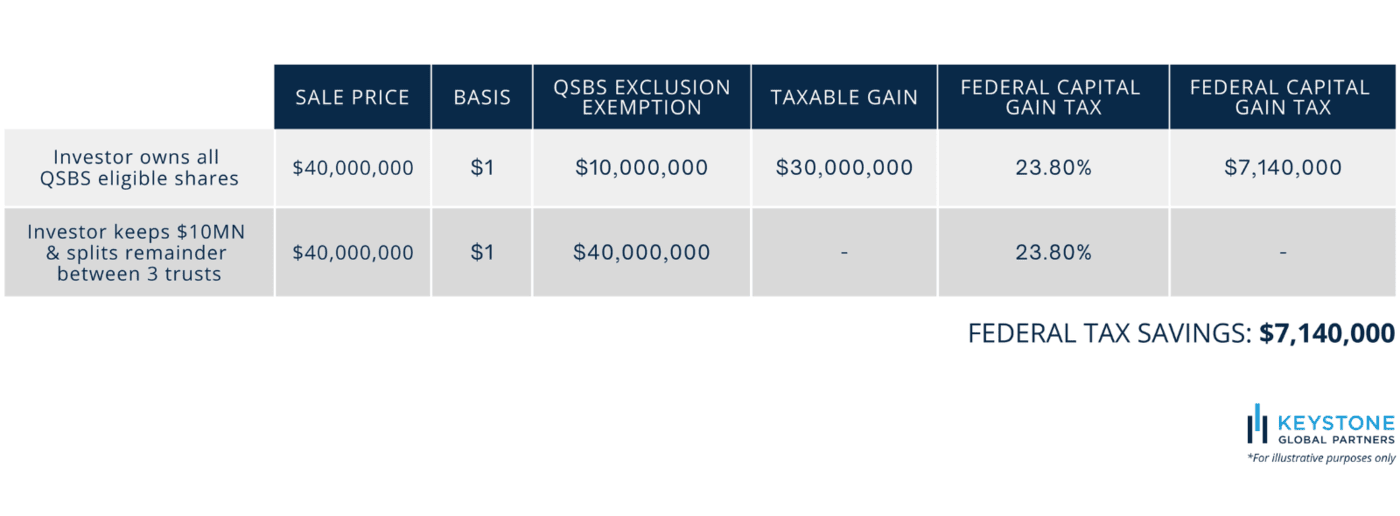

1) Creating additional taxpayers: Trusts “stacking”, gifting, and splitting up your QSBS into different entities

Certain types of trusts can be powerful tools for optimizing QSBS planning. They not only maximize Section 1202 gain exclusions but also assist in federal and state income tax planning, asset protection, and wealth transfer. Since a Section 1202 exclusion is granted per taxpayer, dividing ownership of QSBS among multiple taxpayers through specific trusts can multiply the total exclusion amount per trust.

Founders can utilize a sophisticated approach known as QSBS stacking, which involves gifting Qualified Small Business Stock (QSBS) to irrevocable non-grantor trusts. This strategy allows each trust to qualify for its own $10 million Section 1202 gain exclusion.

As the grantor, founders can designate beneficiaries, such as their children or future generations. If multiple trusts are used, it’s essential to ensure that they are not carbon copies of one another. This prevents you from being treated as a single entity for tax purposes.

For example, consider a founder with three children. By creating a QSBS non-grantor trust for the benefit of each child and transferring $10 million of QSBS to each trust, the founder can effectively exclude $40 million from federal taxes — $10 million through his own 1202 exclusion and $30 million through the trusts.

When gifting QSBS shares to a trust, keep in mind that this will count against your lifetime gift tax exemption of $13.61 million ($27.22 million for married couples). To maximize tax efficiency, it’s wise to execute this transfer well before an exit when asset valuations are typically lower, instead of waiting until the exit is imminent. This proactive timing can significantly enhance the effectiveness of your lifetime gift tax exemption usage.

2) Incorporating appreciated property “packing” to use the 10X basis limitation

Unlike the examples of QSBS stacking above, which aims to increase the cumulative QSBS exclusion above $10 million by adding more taxpayers, QSBS Packing is a tax strategy that seeks to boost your Section 1202 gain exclusion beyond $10 million and up to $500 million per taxpayer. This is done by increasing the basis of your QSBS stock.

Contributing appreciated property is an effective strategy for optimizing the Section 1202 exclusion by leveraging the 10X basis cap to achieve over 10 million per taxpayer. When property is exchanged for Qualified Small Business Stock (QSBS), the tax basis of the QSBS is determined by the property’s fair market value at the time of contribution.

Below are several strategies for QSBS packing that can enhance your tax planning.

Starting a company as an LLC and later converting to a C Corporation

Founders can start their business as an LLC. Once it has value below $50 million, they can convert it to a C corporation.

This approach offers the potential to have a substantial amount of Section 1202 gain exclusion by setting the basis of Qualified Small Business Stock (QSBS) at the LLC’s fair market value at the time of conversion. For instance, converting your LLC to a C Corp with a $40 million pre-money value could potentially exclude $400 million in gains!

However, there are some downsides to this strategy. For example, delaying the five-year QSBS clock can be a drawback. Additionally, waiting to convert may be less beneficial if the company’s growth doesn’t meet expectations. Also, this can be more complicated with investors and employees and more expensive on the legal front.

Contributing cash, IP, or other property to increase your basis.

Another QSBS packing tax strategy involves contributing cash or intellectual property in exchange for QSBS equity, which can effectively increase the basis of your QSBS stock. This approach allows you to exclude a larger amount from capital gains upon selling.

For example, if you contribute $2 million in cash and receive $2 million worth of QSBS stock, your new QSBS basis becomes $2 million. Provided you meet the requirements, you can exclude up to ten times your stock basis, which amounts to up to $20 million of exclusion by leveraging the Section 1202 gain exclusion.

3) Selling QSBS with basis over multiple years

One strategy to maximize the Section 1202 gain exclusion is to spread the sale of Qualified Small Business Stock (QSBS) over multiple years. This is particularly valuable for stockholders with some basis in their shares.

Imagine a scenario where a founder’s company is acquired with a deal structure that includes

- 50% cash upfront

- The remaining 50% in year three (assuming the EBITDA targets are met)

If the founder holds both common founder stock and preferred stock acquired later, they could sell the common stock in the first year and claim up to $10 million through the Section 1202 gain exclusion. In year three, they could then sell the preferred stock and claim an additional 1202 exclusion based on the 10X basis.

4) Selling high-basis and low-basis shares in the same tax year

Another strategic approach involves selling both high-basis and low-basis QSBS stock within the same tax year. This tactic aims to increase the total aggregate basis of your QSBS stock and enables you to exclude up to ten times the aggregate adjusted basis for the 1202 stock sold that year.

For example, let’s assume you own two classes of QSBS 1202 exclusion stock: one with zero basis and another with a $2 million basis that has little or no gain and has been held for just a year. You can sell both in the same tax year to exclude up to $20 million and minimize capital gains tax.

This is achievable even if the high-basis stock has been held for less than five years. It’s a scenario that presents you with some valuable planning opportunities.

5) Reinvesting proceeds of QSBS sales in replacement QSBS under a Section 1045 rollover “tacking”

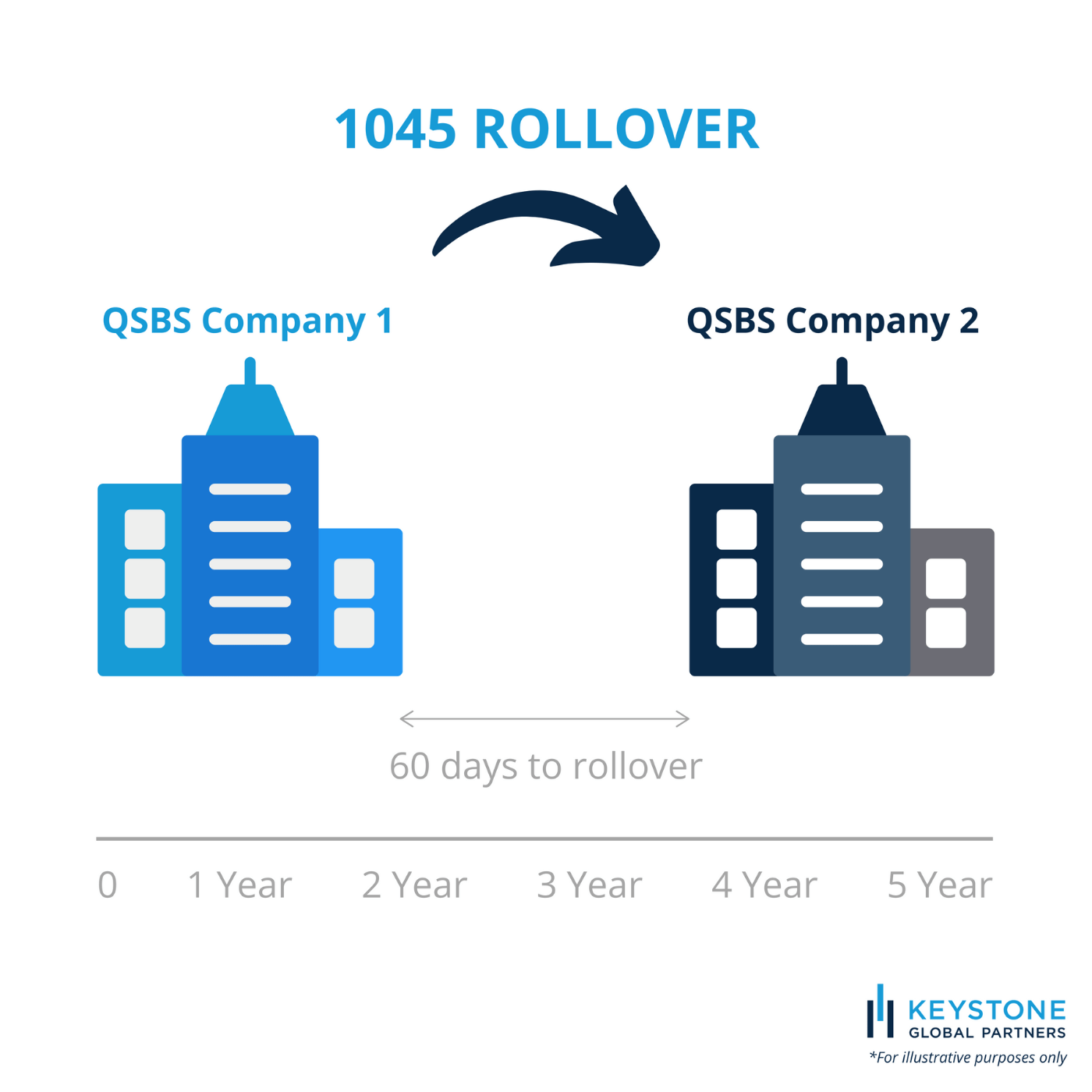

A Section 1045 rollover allows a founder or taxpayer to defer capital gains if their company or Qualified Small Business Stock (QSBS) is sold before the five-year holding period. Additionally, it may completely eliminate these gains if the combined holding periods of the original and replacement company total five years.

This deferral is facilitated by using the sale proceeds to acquire replacement QSB stock within 60 days. You thereby postpone gains from the initial sale of the original QSBS.

1045 rollover strategy: Rolling sale proceeds into replacement QSBS companies

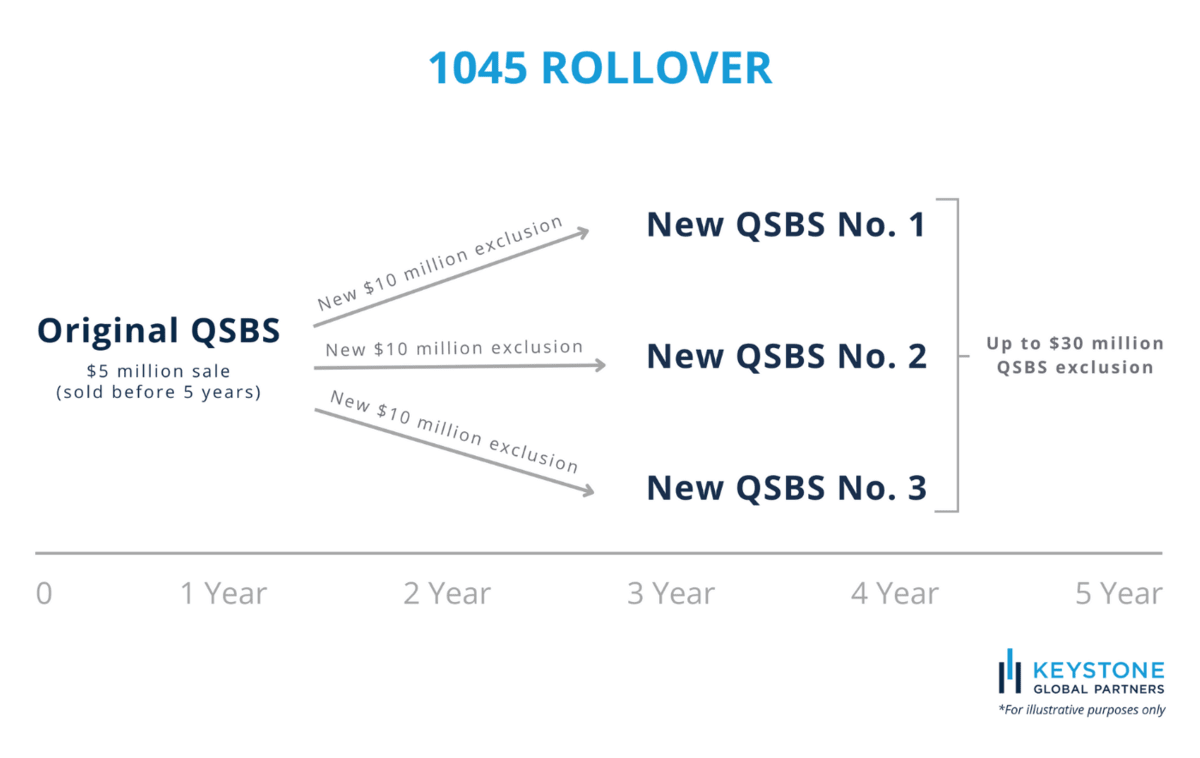

Stockholders can maximize the benefits of a Section 1045 rollover by utilizing the Section 1202 gain exclusion across multiple investments. This strategy involves rolling the sale proceeds from the original QSBS held under five years into several new QSBS-eligible companies.

Doing so allows for a $10 million (or 10 times basis) exclusion for each new investment. See the example below of a founder with a $5-million exit, who rolls everything into three new QSBS-eligible companies.

1045 rollover strategy: Start a new QSBS company

Instead of investing your proceeds into someone else’s venture, it might be the perfect time to pursue your next big idea. For founders eager to dive into another venture soon after an exit, a self-funded approach could be ideal.

Keep in mind the 100 percent rule. If you only roll over part of your sale proceeds, you can only defer a proportional portion of the tax.

Ready to go all-in? To execute this strategy, you’ll need to establish a new C-corp to launch a new QSBS company and roll your sale proceeds into it.

Tip: This QSBS for startup founders’ strategy can also offer a layer of protection. If the business doesn’t succeed, you can wind down the company and potentially qualify for the Section 1202 gain exclusion for any returned funds. This assumes that the holding periods work.

1045 rollover strategy: Acquire a QSBS company

Here’s how it works. You must create a newly formed C-corp and roll the proceeds from the original QSBS into this new entity. This C-corp can then acquire a new QSBS-eligible company.

For the Section 1202 exclusion to apply, the total holding period of the actively engaged new company must be at least 80% of the holding time and include the search period. For instance, if it takes eight months to acquire a company, the actively running QSBS company must have a holding period of 32 months to meet the 80% requirement.

State tax considerations

It’s important to consider state-specific tax laws. Remember, not all states conform to the federal guidelines for the Section 1202 gain exclusion.

Additionally, careful planning is required to ensure compliance with federal estate and gift tax regulations, especially when using trusts or gifting QSBS. For example, California, where many of our founder clients live, does not conform to the federal treatment of QSBS.

As of 2024, the top CA tax rate is 14.4%. We do a lot of planning for our California clients on the state tax optimization front.

Timing

Founders should continuously assess their equity ownership throughout their company’s life cycle. Different strategies may be more effective at various stages depending on the current and projected estimates of what their shares are worth.

A first-time founder’s strategies may differ greatly from a repeat founder’s approach. However, planning should be done well before accepting any formal offer or Letter of Intent (LOI).

Delaying until a deal is inked can lead to substantial tax liabilities due to income assignment. As per the Internal Revenue Code, if all contingencies are cleared and no more deal points are to be negotiated before the closing date, the transaction’s effective date is usually the signing date, not the closing date. Don’t fall into the trap of waiting until the last minute.

Planning around the Section 1202 gain exclusion is not a one-time task and requires an iterative approach. Personal circumstances and future goals also play a significant role in determining the most suitable strategy.

Summing up the Section 1202 gain exclusion

Maximizing the Section 1202 exclusion requires strategic planning and a thorough understanding of the relevant tax regulations. Hopefully you can leverage the variety of strategies that we’ve discussed and successfully implemented with our founder clients.

At the same time, it’s important to note that not everyone has the same opportunities and circumstances. Therefore, effective tax strategies planning must be tailored and customized.

Always consult a tax advisor to adapt these strategies to your specific situation. Doing so will ensure you comply with applicable tax laws wherever you live.

By skillfully navigating the intricacies of the Section 1202 gain exclusion, startup founders can fully leverage this valuable tax benefit. This can potentially lead to saving millions in federal income taxes.

If you’re a founder, I hope that you take advantage of it, given the blood, sweat, and tears that go into starting and running a company. The original purpose of the Section 1202 gains exclusion was to reward both founders and investors of small businesses, support the entrepreneurial ecosystem, and create jobs.

FAQs

Which Section 1202 gains are eligible for 100% exclusion?

QSBS held for over five years can qualify for the Section 1202 gain exclusion if the stock is issued by a domestic C corporation on or after September 28, 2010. Additionally, the corporation must meet specific gross asset and active business criteria both at the time of issuance and throughout the holding period. There are a few other QSBS Eligibility requirements as well.

What is the maximum gain exclusion?

Under Section 1202, the maximum gain exclusion is the greater of $10 million or ten times the adjusted basis of the Qualified Small Business Stock (QSBS) sold. If your adjusted basis in the stock is below $1 million, you can exclude up to $10 million from your taxable income.

Meanwhile, if your adjusted basis exceeds $1 million, you can exclude up to ten times that amount. In theory, a taxpayer could achieve a maximum gain exclusion of just under $500 million if they have an adjusted basis of right under $50 million and subsequently sold their stock for more than $500 million or more.

Is there a requirement for a holding period for QSBS?

Yes, there is a five-year holding period requirement for QSBS. Some who have exited before it ends may consider using a 1045 rollover strategy to “tack” the holding period from the sold QSBS to the new QSBS.

What are the potential state tax considerations for Section 1202 gain exclusion?

It’s important to note that not all states conform to the federal guidelines of the Section 1202 gain exclusion. Additionally, careful planning is required to comply with federal estate and gift tax regulations when using trusts or gifting QSBS.

California, where many of our founder clients reside, does not conform to the federal treatment of QSBS. As of 2024, the top CA tax rate is 14.4%, which makes state-specific planning crucial.

When should founders start planning for their Section 1202 gain exclusions?

Founders should continuously assess their equity ownership throughout their company’s life cycle. Different strategies may be more effective at early, mid, or late stages depending on the current and projected estimates of what their shares are worth.

However, planning should be done well before accepting any formal offer or Letter of Intent (LOI). Planning around the Section 1202 exclusion is not a one-time task and requires an iterative approach that involves consideration of personal circumstances and future goals.

How do I report the Section 1202 gain exclusion on my tax return?

Reporting the 1202 exclusion on your tax return is essential for maximizing your benefits and ensuring compliance with IRS guidelines. This process requires thorough documentation of any Qualified Small Business Stock (QSBS) sales and involves completing Form 8949 and Schedule D. We recommend collaborating with an accountant to ensure accurate reporting.